Well, not that lot, but the status quo as far as buy-to-let is concerned.

I’ve let the dust settle for a week or so before commenting upon the latest round of the Chancellor’s assault on buy-to-let investors (as that is what it’s becoming), mostly because there’s been an awful lot of other commentary around and we need time to absorb the full impacts before rushing around & jumping to conclusions.

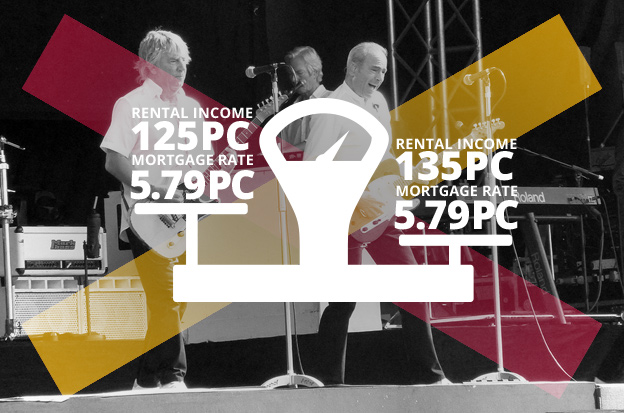

This also allowed the real major issue of the week to emerge: Barclays became the first major lender to announce an increase in the rental cover requirement they levy in order to approve a buy-to-let loan. Where previously Barclays required landlords to have a rental income of 125pc of the monthly interest, calculated at a mortgage rate of 5.79pc, it has increased this to 135pc at 5.79pc.

This was bound to come, and it will be no shock to see most other lenders tighten their criteria in a similar fashion. If the income generated by the rental declines as a result of tax hikes, landlords will have greater affordability constraints applied at the outset to the amount they can actually borrow. Of course, this is happening now, not in two to six years’ time as the new tax rules come into play, so it is a sign of worsening sentiment towards investor landlords with b-t-l loans.

I recall opening the doors of my letting agency in the early noughties and being surprised how many landlords walked in with 85% loans-to-value along with rather steep assumptions of the available rent in the locality. Even if somewhat inflated rent expectations could ever be met, an 85% ltv meant the prospects of covering the mortgage from the rent were pretty much dead in the water from the off. It’s only right that times have changed in the intervening period. But I never used to feel that a mortgage was something to be feared (in fact quite the reverse, because of the “miracle of gearing”) as long as you had the loan-to-value level right, i.e. the loan at a low enough level for the rental cover to provide for the ups and downs of this game (unless you were on Northwood’s totally certain Guaranteed Scheme, I feel bound to add).

But now, the situation is totally different. As the Telegraph rather alarmingly but probably accurately puts it: http://www.telegraph.co.uk/finance/personalfinance/investing/buy-to-let/12027732/Buy-to-let-investors-will-need-50pc-deposit-or-no-mortgage.html?utm_source=dlvr.it&utm_medium=twitter

So, status quo is now wildly different. I only wish that were true of Status Quo…

Fabulous news: Remember simple maths: The less people that own multiple homes the more of us that can own one home of our own. This hopefully means a less greedy fairer society where the needs of the millions of Renters and First Time Buyers priced out of a decent home are put ahead of multiple home owning Buy to Let landlords and Buy to Leave investors. Remember houses should be primarily treated as homes to be lived in not as assets for the capital rich to get ever richer. At last the government is taking a step in the right direction.

LikeLike

Thanks Toffer, good points there!

LikeLiked by 2 people